The job of auditors has always been interdisciplinary. At the core of the auditor’s professional development is a multitude of disciplines—including accounting, taxation, risk management, forensics and business—and skills related to information systems, communication, teamwork and project management. These have been vital in building success in an auditor’s role. At its very core, the profession recognizes the multidisciplinary nature of its accountability.

Today’s interdisciplinary auditors are no different, except that what might have been termed peripheral disciplines (e.g., information technology, forensics, data analytics) have become critical prerequisites to effective role playing. For example, the cloud computing environment makes the task of verifying transactions and testing controls more challenging, and the emergence of voluminous qualitative and quantitative data pushes the auditors to creatively analyze information to corroborate what they observe from the traditional financial transactions.

Disruptive technology, competitive forces and changing consumer preferences—in part due to the technological revolution—have forced businesses to dynamically search for and respond to emerging strategic gaps in their business models. Walmart and Target, for example, strive to calibrate their online sales avenues as Amazon shows greater strength in its consumer-friendly, innovative reach to markets. This changes the very face of the business that the auditor is tasked to audit. While existing businesses may change dramatically, businesses such as Facebook, Twitter and LinkedIn emerge with a very different social structure bonded with their revenue generation processes. Because auditors audit transactions, and transactions vary with the underlying business model, the context is as critical as the content central to the auditor’s assurance.

Without a good understanding of the business drivers in place, the auditor would be ineffective in delivering his or her promise. For delivering value, the auditor must keep up with not just financial accounting and reporting standards and auditing standards, but also with all relevant peripheral disciplines. Take, for example, fair value measurement of intangibles and intellectual property. “The newer class of intangibles and intellectual property assets raises varied and less understood valuation challenges.”1 In recent years, business valuations for fast-growing start-ups could be fairly detached from the current or future profitability of the business. As more businesses enter or prepare to enter the public domain, it is critical for auditors to develop and support their valuation judgment. Sure enough, most complex audits are a team effort; in fair value measurement, for example, the auditor may employ or engage an appraiser. Thus, the lead auditor may recruit team members strong in disciplines where he or she might not be hands on. But this does not exempt the lead auditor from having a good understanding of what goes on underneath and how this creates new risk or changes the existing ones.

Professions Change

With few exceptions, almost all professions change over time, perhaps not so much in their basic discipline, but rather because of peripheral disciplines emerging or changing in the overarching domain of their accountability. Civil engineering, for example, is impacted by innovation in building materials and new ways of making structures earthquake resistant. Human resource management is changing as innovative processes take over the monitoring and feedback requirements of the hiring value chain. Suppliers and consumers are impacted by drone delivery options, and the Uberization of local delivery services competes in the same space. Those in the military cannot deny the need for deployment of drones in their missions and those in the taxi business must confront Uber-like options that appear to be more efficient in delivering services to patrons.

Not only do professions change over time, but the rate of change in some professions has accelerated considerably. Much of what is impacted is not the basic mission of the profession or philosophy—the value proposition—behind it, but rather how to accomplish the objectives given the changes that are here or forthcoming. Civil engineers, for example, work with new environment-friendly materials while ensuring that the objective of protection from natural disasters is achieved in their projects. And hardware and software engineers want to leave no known loopholes for hackers to compromise the systems they build while making their products usable in shared settings. Electrical engineers fight the new threats of attackers remotely shutting down power grids, leaving communities without electricity.

As things change, every profession should take into consideration how change could make their jobs more efficient, more productive and how they achieve better outcomes. Change can be good if it is embraced with a vision and openness to change; it may render the profession less valuable if considered outside of the professional boundaries and, thus, having nothing to do with the accountability of the profession.

What Changes for the Auditor?

Auditors are discovering that their roles are changing as well. As providers of assurance, the scenarios impacting change in risk have multiplied in newness, number and complexity. It seems it was much easier to comprehend clouds than it is the blockchain platform. The impact of artificial intelligence (AI) is pervasive.2 Driverless cars present a more challenging risk environment than the traditional, but smart, cars preceding the impending change.3 To know an emerging risk requires one to first know the environment, processes affected and how they might be affected.

Besides technology, the sheer volume of qualitative and quantitative data available to the auditors is increasing at an unprecedented rate. Combining such data to create insights never before possible is challenging and yet is an incontrovertible task for auditors. Creativity and analytical capabilities come from different parts of the brain. While accountants and auditors are seen as analytical, those who can use the whole brain in an audit could become front-runners in the race for survival and growth as a professional.

While hybridization of right brain-left brain4 might sound new to the profession, some tasks in the auditing profession have required the use of the whole brain, so the experience is not totally new. For example, the idea of brainstorming implies a deep reflection on both quantitative and qualitative data about people, culture, results and behaviors. And forensic audits often engage in soft data as well to find patterns that might corroborate with the pictures emerging from hard data. What has changed, however, is potentially greater use of the right brain where creativity likely emerges. Perhaps not every auditor will show equal promise to rise to this challenge. Those who do are likely to be the front runners in the field and may command a longer tenure or higher compensation. In career building, as always, the choice is: Be a dated professional who is good in traditional roles or a savvy professional with can-do confidence in the technology-driven businesses. Requirements from a recent job posting for the position of an auditor, who is responsible for providing support of the Corporate Audit Data Analytics Program, integrating data analytics and continuous auditing/monitoring into corporate audit processes include:

- Understand data sources (systems) to effectively extract data relevant to assigned objectives

- Document code logic, procedures performed, testing results, issues and recommendations

- Hold working knowledge of data analysis and extract, transform, load (ETL) software

- Execute scripts, queries and reports primarily through the use of Structured Query Language (SQL), access control list (ACL) and Tableau

- Experience with Visual Analytics (analytical reasoning facilitated by interactive visual interfaces)

- Analyze data from multiple systems and sources to ensure that audit teams act proactively on transactional trends and exceptions

- Analyze large data populations for unusual activity, data integrity and facilitate control testing

- Ability to consolidate information from a variety of sources and present information clearly and concisely

Changing Audit Roles

While this may not be a job for every successful auditor, it points to the changing nature of the environment in which future audits will take place. Consequently, a good understanding of how to confidently evaluate the work of an expert in data analytics, for example, is a must for today’s auditors.

Another wave of change in auditors’ roles comes from blockchain technology.5 The growing number of applications will affect organizations, both for profit and nonprofit, that seek to maintain accurate, but anonymous, records of transactions. Adoption of such technologies by an organization, even at a transaction level, would simply mean its auditors will have to prepare for assessing attendant risk.6 Additionally, in data-driven economies, a reasonably sophisticated understanding of privacy, data encryption and public key infrastructure (PKI), etc., comprise an important knowledge prerequisite. This is especially important since large organizations are now virtually linked to their suppliers and customers, and the weakest link in the third-party network could create significant cyberrisk for the auditee.

And while not all changes will impact every organization equally, there are enough pervasive, disruptive technologies that could impact practically every entity, regardless of size or location. This is in large part due to a common thread, the Internet, that reshapes every heretofore isolated resource. The Internet of Things (IoT), for example, is the creation of a network connecting everything to everything across organizations and people. Cloud computing as a technology has settled somewhat, but still has the steam to change the view of technology platforms and applications in almost any organization, regardless of size.

Assurance implies trust, a function of competency and independence. Competency in a broad sense may be the same for every professional, but it takes shape within the context of what the employer organization (or the auditee) does. One might be a perfectly good auditor, but in a certain context where current knowledge in technology or industry expertise is low, you may be frustrated and not as productive as you are generally. So, the measure of competency, even with the same employer, could change considerably over time, especially in today’s disruptive environment.

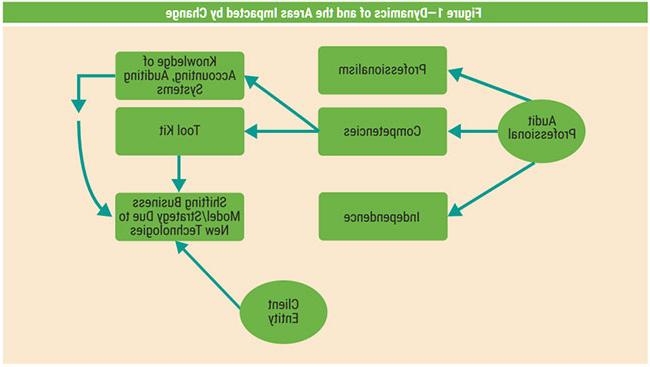

Figure 1 shows the dynamics of and areas impacted by change. Note that while the bedrock of professionalism is not impacted by the change, ethical dilemmas emerging from change can be expected to be vastly different, and this may result in ethical blind spots.

Accountability for Career Trajectory

It appears that rapid change will dwarf the traditionally valuable competencies in comparison to new things one must learn to stay viable. The business of identifying risk is contingent upon the comprehension of events that trigger risk. Knowing the fundamental nature of the technology and its variations should help.

In putting fundamental skills and best practices to use in new settings, auditors must be creative. The traditional thought that accountants must not practice “creative accounting” could be misleading. Sadly, this notion has more to do with the misuse of the word “creative,” as in manipulation of numbers to commit a compromise. Indeed, accountants and auditors have been creative in their work to produce efficiency, help businesses perform better and develop better ways to assess risk.

While there may be several sources to tap such knowledge, some are obvious. One is the professional continuing education requirement, which can be met by using programs, workshops, webinars, and presentations on emerging technologies and their applications. Learning by doing is more effective than learning through listening or reading; therefore, workshops that involve hands-on exercises should help greatly in learning the material and, more important, in gaining confidence in what one knows upon the completion of such training. Since not everything can happen on the employer’s watch, one must consider self-study and programs and events outside of the normal day-to-day work. Courses in data analytics, for example, are now available for auditors to enhance their skills.

To have been licensed as a professional auditor is no guarantee of required capabilities in the future. For this, one must seek every possible opportunity to embrace what may appear to be difficult, new or outside the range of one’s current tasks. The default option is to do nothing, which may mean one’s degradation in future potential as an auditor. A counter argument to this line of thought is also important to note here: Most audit engagements are essentially a team effort; as long as someone knows about the new technology and its applications, others may not need to know it. This is indeed true, however, some baseline knowledge of the system that processes transactions is important to contribute as a team member. With limited knowledge of the frontiers of technology and their applications, the affected individual can only contribute in a limited manner and, consequently, may even be ignored by others on the team.

As for employers, the question is equally important. The job market for auditors is tight. Perhaps they should look to recruit from other disciplines such as computer science and train the recruits in auditing. This may not necessarily lead the recruits to pursue professional certification in auditing. An alternative is to look within the organization for employees with potential to do well as auditors. The downside here is that these employees who thrived in other roles may not find the auditor’s role attractive. Having a sophisticated internship program could prove valuable in finding individuals with capabilities sought by the organization. Finally, for the current pool of auditors, encouraging or even requiring some of them to take selected training programs funded by the organization can help.

Ultimately, the accountability for shaping one’s professional career rests with the individual. It is very likely that the profession would promote and encourage avenues for keeping its members current in the changing tool kit of competencies. However, seizing such opportunities is only in the hands of the professional auditor. The only other option to force some degree of currency on the members is for the profession to impose a periodic board examination, much like those in the medical profession.

Endnotes

1 Sondhi, A.; M. Bullard; N. Harrison; L. Shover; R. Tarola; L. Turner; G. Walsh; “Report From the Working Group on PCAOB Publications,” Public Company Accounting Oversight Board, 2015, http://pcaobus.org/News/Events/Documents/09092015_IAGMeeting/Publications_Slides.pdf

2 Deloitte, Artificial Intelligence, Innovation Report, 2018, http://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/Artificial-Intelligence-Innovation-Report-2018-Deloitte.pdf

3 Raval, V.; M. J. Dentlinger; “Risk Landscape of Autonomous Cars,” EDPACS, vol.56, iss. 3, 3 November 2017, p. 1-18, http://www.tandfonline.com/toc/uedp20/56/3?nav=tocList

4 Burning Glass Technologies, The Hybrid Job Economy: How New Skills Are Rewriting the DNA of the Job Market, January 2019, http://www.burning-glass.com/wp-content/uploads/hybrid_jobs_2019_final.pdf

5 Brender, N.; M. Gauthier; “Impacts of Blockchain on the Auditing Profession,” ISACA Journal, vol. 5, 2018, http://h04.v6pu.com/resources/isaca-journal/issues

6 Cangemi, M. P.; G. Brennan; “Blockchain Auditing—Accelerating the Need for Automated Audits!” EDPACS, vol. 59, iss. 4, 4 June 2019, p. 1-11, http://www.tandfonline.com/toc/uedp20/59/4?nav=tocList

Vasant Raval, DBA, CISA, ACMA

Is an emeritus professor of accountancy at Creighton University (Omaha, Nebraska, USA). The coauthor of two books on information systems and security, his areas of teaching and research interests include information security and corporate governance. He can be reached at vraval@creighton.edu.

Prapti Acharya, CA

Is a chartered accountant based in Singapore for the last 11 years. She has been advising businesses on cross-border investment and operating models from the tax perspective for the last 20 years with a recent focus on mergers and acquisitions, predominantly in the Asia Pacific region. She can be reached at prapti.acharya@gmail.com.