The fintech industry is growing at such a fast pace1, 2 that investors, boards of directors, senior management and government regulators need to reexamine current practices and models of fintech governance. One well-known example of this growth is the US$16 billion invested in the UK fintech industry in the first half of 2018. This represented more than 25 percent of the US$57.9 billion invested in the fintech industry worldwide.3 The bigger the fintech industry gets, the more important it is to have suitable governance mechanisms in place.

The Fintech Revolution and Governance

Fintech enterprises are transforming financial systems all over the world. In fact, these enterprises have a mandate to sustain an effective and efficient technology-oriented fintech bionetwork to provide crystal-clear financial transactions. The main idea behind this groundbreaking industry is to make financial services available to everyone everywhere, constituting a real “fintech revolution.”4

The demand for fintech governance practices is increasing on a daily basis and governance has become a critical success factor throughout the fintech industry.

Etymologically, governance can be traced back to the Greek verb kubernân (to pilot or steer). The Greek term gave rise to the medieval Latin gubernare, which has the same connotation of piloting, rule-making or steering.5

In terms of a fintech enterprise, there are three elements to the previous definition. The first element is piloting, which has to do with sponsoring and taking ownership of a fintech organization. The second element deals with rule making, which entails setting out the rules of engagement to be used by the fintech team. The last element deals with steering, which has to do with guiding, maneuvering and driving the fintech team to a secure place.

At this stage, it is important to underline that fintech risk management provides the foundation for managing fintech governance.6 An example is the managing of regulation-related risk factors such as those inherent in Comprehensive Capital Analysis and Review (CCAR), the US Dodd-Frank Act, the EU General Data Protection Regulation (GDPR), the Basel Markets in Financial Instruments Directive (MiFID) and the Revised Payment Service Directive (PSD2).7

Fintech enterprises are facing multiple governance challenges around the world. For instance, many of them have international customer bases and are obligated to meet government regulatory requirements, including those related to money laundering, data protection, privacy, and bribery and corruption, in several jurisdictions.8

Fintech Governance Challenges

Before demonstrating how to approach fintech governance, it is appropriate to address some of the governance issues currently facing fintech enterprises worldwide (figure 1):

Before demonstrating how to approach fintech governance, it is appropriate to address some of the governance issues currently facing fintech enterprises worldwide (figure 1):

- Issue 1: Younger and private enterprises with lack of financial stability—Many fintech enterprises are young, private organizations driven by innovation, and they lack the financial strength necessary to attract new clients and partners. This represents a trust issue that requires immediate attention from the governance team if the enterprise is to stay afloat.

- Issue 2: Alignment of new governance practices with fintech enterprises—Because of the agile nature of fintech enterprises—which operate in a global environment, implementing new technologies under multiple legislative schemes—it is essential that they institute new governance practices to sustain the evolution of the fintech enterprises.

- Issue 3: Active investors—Fintech active investors take on the roles of advisors and consultants to fintech enterprises. Therefore, it is recommended to include fintech active investors on the enterprise’s governance team.

- Issue 4: Regulatory requirements across multiple jurisdictions—Because many fintech enterprises have international client bases, they are required to comply with government regulations across multiple jurisdictions. Therefore, proper governance support should be available for this new type of organizational environment.

- Issue 5: Innovative solutions around risk and regulation mandates—Government regulations have allowed fintech enterprises to build solutions around risk factors and regulatory requirements. Therefore, governance support should be available to guide the fintech enterprises in this effort.

- Issue 6: Lack of governance mechanisms on implementation of new technologies—Because fintech enterprises are oriented toward implementing cutting-edge technologies to produce innovative solutions, they need to have suitable governance processes in place to implement such technologies and roll out state-of-the-art solutions—for instance, having delineated a governance process to implement distributed ledger technology (DLT) for an Ethereum application.

Fintech Governance Levels

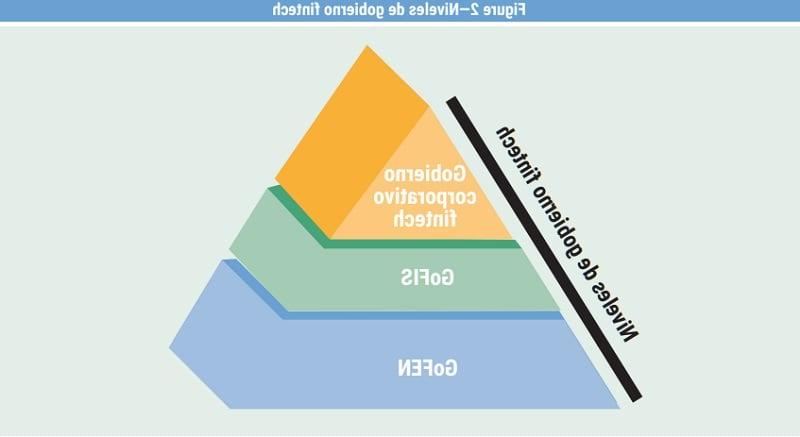

Governance can be studied from different angles, such as corporate governance, enterprise governance and IT governance perspectives.9 It can be helpful to focus on three levels of governance: fintech corporate governance, governance of fintech innovative solutions (GoFIS) and governance of fintech enterprise (GoFEN), as depicted in figure 2.

Fintech Corporate Governance

This is the highest level of governance of a fintech enterprise. It is where the shareholders, boards of directors (BoDs), enterprise management, government agencies (regulators) from multiple jurisdictions, active investors, fintech technology partners and other stakeholders interact to create a balance of power within the fintech enterprise. These participants can be thought of as the seven blades that propel fintech corporate governance. The main objective of the fintech corporate governance level is to establish a governance mechanism to oversee the “system of structural, procedural and cultural safeguards designed to ensure that a company is run in the best long-term interests of its shareholders.”10 However, in terms of investment management, fintech corporate governance enhances the “long-term investment returns, mitigating risks and providing a better picture of portfolio companies.”11

Adapting the definition of “corporate governance” provided by the Organisation for Economic Co-operation and Development (OECD), fintech corporate governance can be defined as:

A set of relationships between a company’s management, its board of directors, its shareholders, its active investors, government agencies from different countries, its fintech technology partners and other stakeholders. Fintech corporate governance also provides the structure through which the objectives of the company are set, and the means of attaining those objectives and monitoring performance are determined.12

Corporate governance is “one key element in improving economic efficiency and growth as well as enhancing investor confidence.”13 In that sense, fintech corporate governance and corporate governance have the same goals.

As a result, an analysis of the definition of fintech corporate governance reveals that there are nine elements:

- Fintech enterprise management—Responsible for day-to-day operations

- BoDs—Oversees the entire enterprise; elected by the shareholders

- Shareholders—Owners of the enterprise

- Active investors—Organizations or individuals who put money into the fintech enterprise to gain profits in return; active investors also provide strategic guidance

- Government agencies—Entities that operate as financial regulators in their jurisdictions

- Fintech technology partners—Includes fintech start-ups and technology developers

- Other stakeholders—Financial customers and traditional financial institutions, among others

- Fintech corporate governance structure—Supports the objectives of the fintech enterprise

- Monitoring and control functions—Evaluates the fintech enterprise’s performance and help it realize its objectives

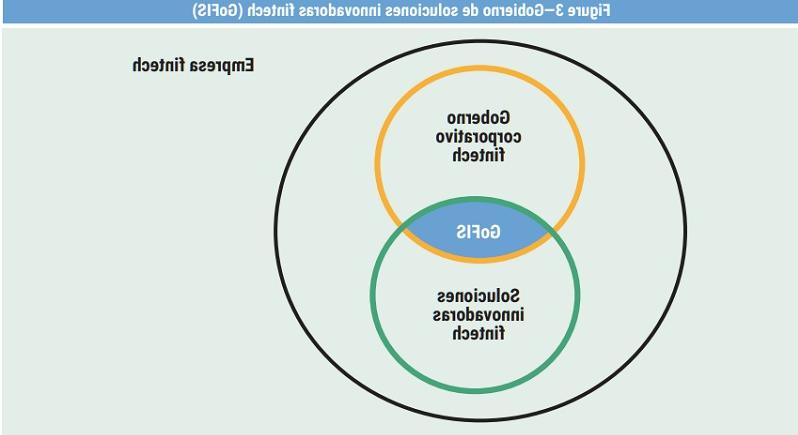

Governance of Fintech Innovative Solutions (GoFIS)

This is the level where governance is applied to the development and implementation of the following types of innovative solutions:14, 15

- New business models—A business model is a blueprint for producing revenues at an acceptable cost, including assumptions about how to create and capture value.16 Examples of fintech business models are:17

- Wealth management

- Crowdfunding

- Lending business

- Capital market

- Insurance services business

- Applications—An application is a software developed to solve a specific business or technical problem. Examples of fintech applications are:

- PayPal

- Google Wallet

- Airtm

- Venmo

- Skrill

- Uphold

- Processes—A process is a “set of activities designed to accomplish a specific objective by taking one or more defined inputs and turning them into defined outputs.”18 The following are some examples of fintech processes:

- Donation-based crowdfunding

- Insurance claims processes

- Payment processes

- Healthcare billing processes

- Products—A product is a “solution or component of a solution that is the result of an initiative.”19 Some examples of fintech products are:

- Mobile products such as:

– MTN Mobile

– Nequi

– DaviPlata

– Mpesa - Cryptocurrency products such as:

– Bitcoin

– Litecoin

– Ethereum

– Dai

– Monero

- Concept generation

- Concept/project evaluation

- Development

- Launch

- Mobile products such as:

- Services—A service is an “act of helpful activity.”21 In that sense, fintech enterprises provide services to financial clients, including:

- Credit scoring

- Fintech robo-advisory services

- Peer-to-peer (P2P) transfer

GOFIS IS THE INTERSECTION OF FINTECH CORPORATE GOVERNANCE AND FINTECH INNOVATIVE SOLUTIONS.

At the GoFIS level, innovation plays an important role in generating revenues. In addition, GoFIS supports the fintech enterprise’s implementation of strategy. As illustrated in figure 3, GoFIS is the intersection of fintech corporate governance and fintech innovative solutions.

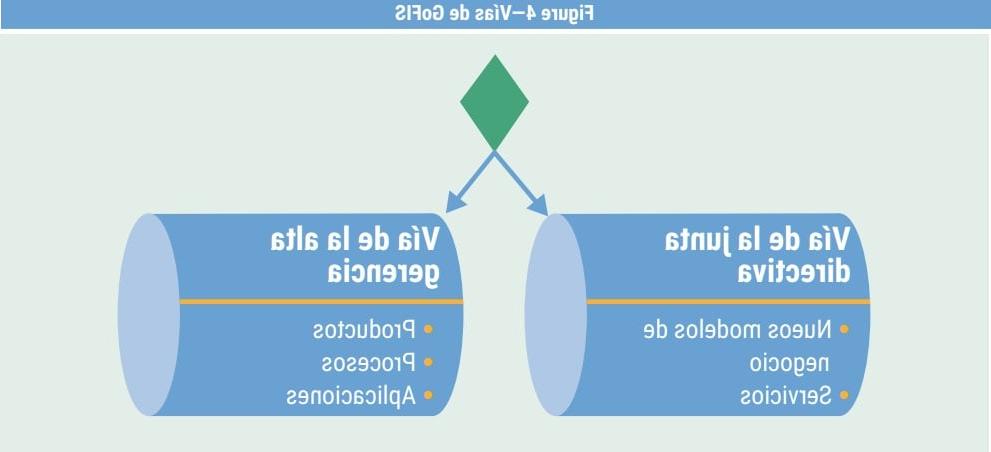

As depicted in figure 4, there are two verticals governance tracks within a GoFIS method: the board track and the senior management track. Before discussing these tracks in more detail, two additional concepts must be defined: “accountability,” which is a “person or group who has the authority to approve or accept the execution of an activity”22 and “responsibility,” which requires a “person who must ensure that activities are completed successfully.”23

Board members are accountable for the development and implementation of new business models or services. Likewise, assigned program managers are responsible for the successful development and implementation of new business models or services.

In the senior management track, selected senior managers, such as a chief executive officer (CEO), chief financial officer (CFO), chief information officer (CIO) or chief operating officer (COO), are accountable for the development and implementation of products, processes or applications. Similarly, assigned project managers are responsible for the successful development and implementation of the designated products, processes or applications.

After the development and implementation of fintech innovative solutions, the next phase is the operation stage. This requires the appointment of operations managers responsible for the daily running of the fintech implemented solutions business (FISB), including profit and loss. Likewise, senior managers must be assigned to and made accountable for the day-to-day functions of the FISB.

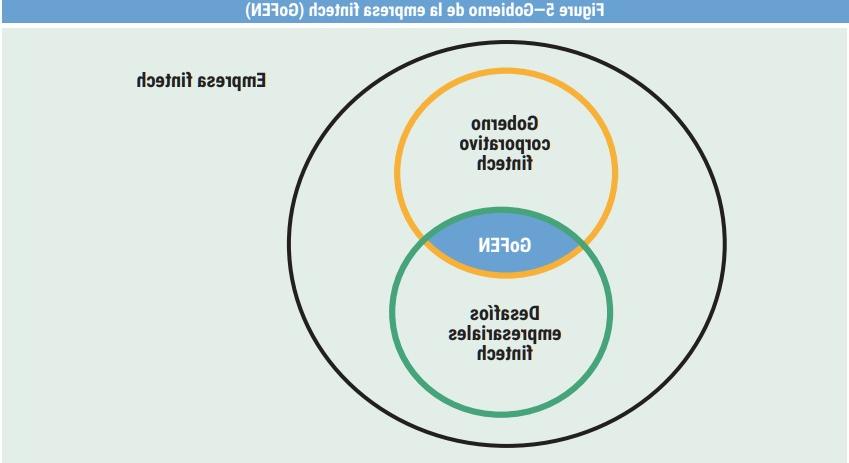

Governance of Fintech Enterprise (GoFEN)

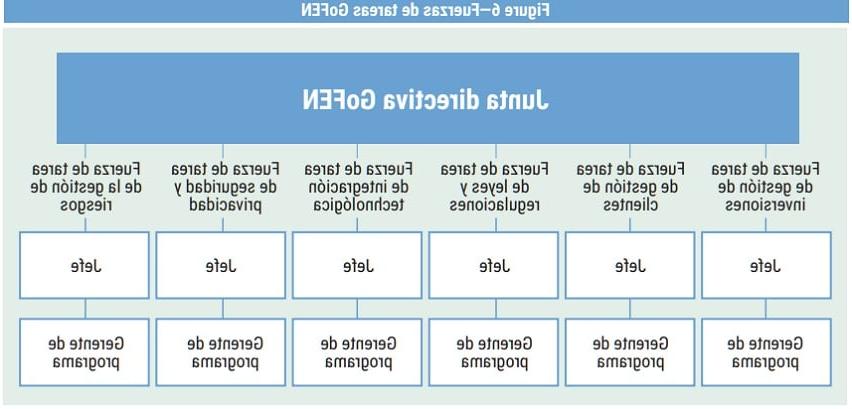

This is the level where governance is applied to fintech enterprise challenges, namely, investment management, customer management, regulation, technology integration, security and privacy, and risk management.24 As illustrated in figure 5, GoFEN is the intersection of fintech corporate governance and fintech enterprise challenges.

At this level of governance, the BoD and senior management make up a GoFEN executive board to oversee the challenges confronting the fintech enterprise. Likewise, six task forces are established, and two roles are defined in each task force: head and program manager. The head is either a board member or a senior manager, and the program manager reports to the head (figure 6). As a result, the head is accountable, and the program manager is responsible for tackling the corresponding fintech enterprise challenges.

Conclusion

There are three important fintech governance levels to focus on: fintech corporate governance, GoFIS and GoFEN. Within GoFIS, there are two vertical tracks of governance: the board track and the senior management track. Similarly, there are six governance task forces that are a part of GoFES: investment management, customer management, regulation, technology integration, security and privacy, and risk management practices. Fintech organizations must have a robust fintech governance program. Effective fintech governance can increase investors’ confidence levels and can maximize the growth of fintech organizations.

Endnotes

1 PricewaterhouseCoopers (PwC), Redrawing the Lines: FinTech’s Growing Influence on Financial Services, USA, 2017

2 Barclay Simpson, FinTech: Growth Versus Governance, UK, 2018

3 Ibid.

4 London Business School, “The Fintech Revolution,” London Business School Review, vol. 26, iss. 3, 2015, p. 50–53

5 Kjaer, A. M.; Governance: Key Concepts, Polity Press, UK, 2004

6 Alvarez-Dionisi, L. E.; “A Fintech Risk Assessment Model,” ISACA® Journal, vol. 3, 2020, http://h04.v6pu.com/archives

7 Op cit PricewaterhouseCoopers

8 Op cit Barclay Simpson

9 Hamaker, S.; “Spotlight on Governance,” Information Systems Control Journal, vol. 1, 2003, p. 15–19

10 Fombrun, C. J.; “Corporate Governance,” Corporate Reputation Review, vol. 8, iss. 4, 2006, p. 267–271

11 Deane, S.; “Corporate Governance: From Compliance Obligation to Business Imperative,” The Corporate Governance Advisor, vol. 14, no. 4, 2006, p. 13–20

12 Organisation for Economic Co-operation and Development (OECD), OECD Principles of Corporate Governance, France, 2004

13 Ibid.

14 Schindler, J.; “FinTech and Financial Innovation: Drivers and Depth,” Finance and Economics Discussion Series 2017-081, Board of Governors of the Federal Reserve System, USA, 2017, http://doi.org/10.17016/FEDS.2017.081

15 Financial Stability Board (FSB), FinTech and Market Structure in Financial Services: Market Developments and Potential Financial Stability Implications, Switzerland, 2019

16 Brandenburger, A.; S. Harborne Stuart; “Value-Based Business Strategy,” Journal of Economics and Management Strategy, vol. 5, 1996, p. 5–25

17 Lee, I.; Y. J. Shin; “Fintech: Ecosystem, Business Models, Investment Decisions, and Challenges,” Business Horizons, Kelley School of Business, Indiana University, USA, vol. 61, 2018, p. 35–46

18 International Institute of Business Analysis (IIBA), Business Analysis Body of Knowledge (BABOK), Canada, 2015

19 Ibid.

20 Crawford, M.; A. Di Benedetto; New Products Management, McGraw-Hill Education, USA, 2014

21 Dictionary.com, “Services,” http://www.dictionary.com/browse/services

22 ISACA®, COBIT® 2019 Framework: Governance and Management Objectives, USA, 2018, http://h04.v6pu.com/resources/cobit

23 Ibid.

24 Op cit Lee, Shin

Luis Emilio Alvarez-Dionisi, Ph.D.

Is a financial technology (fintech), project management and medical informatics professor and an international management consultant. He has provided advisory services to chief executive officers, boards of directors and senior management of Fortune 500 companies and consulted on project, program and portfolio management with numerous enterprises worldwide, including Intel, IBM, Merck, Chevron, Isuzu, Smiths Detection, the Beijing 2008 Olympic Games, Citibank, Standard Chartered Bank and the Government of Singapore Investment Corporation (GIC). His research focuses on fintech risk management, fintech robo-advisory consulting, fintech governance structures, fintech start-up fundraising, project management trends and tuberculosis management information systems (MIS). He can be reached at dralvarezdionisi@protonmail.com.