Cyberattacks are emerging faster than ever in the wake of the COVID-19 pandemic. As new dimensions are incorporated into these disruptive cyberattacks, enterprises around the world must be more vigilant about protecting their critical information assets. Chief information security officers (CISOs), chief information officers (CIOs) and chief executive officers (CEOs) are continually working to identify more effective ways to prevent their enterprises from falling victim to these dynamic threats. By the end of 2020, global cybersecurity and cyberinsurance spending was projected to reach US$124 billion.1 Cyberinsurance has become an important element of the loss recovery measures instituted after a cyberattack. It covers the potential financial losses caused by cyberattacks and the costs of digital forensic investigations and lawsuits following an attack.

Blanket Bond Insurance Contracts

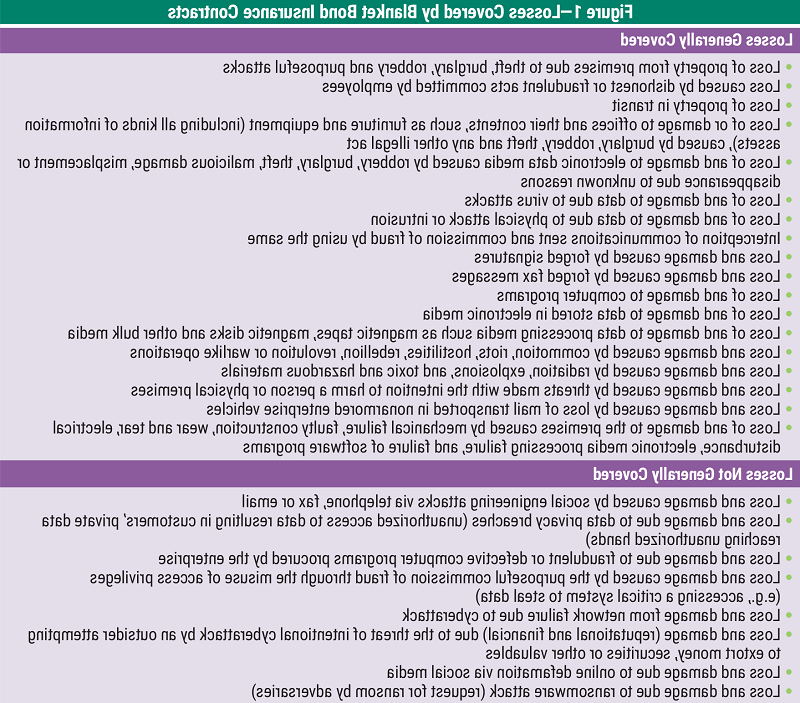

In general, enterprises purchase blanket bond insurance contracts to cover potential losses caused by any man-made or natural disasters. Figure 1 lists the various losses covered (and not covered) by blanket bond insurance contracts based on comparative analysis of cyberinsurance offerings from various insurance firms offering cyberinsurance contracts against blanket bond insurance contracts of sampled organizations.

Figure 1 illustrates the gaps between blanket bond insurance contracts, which provide only partial protection against cyberattacks, and exclusive cyberinsurance liability contracts, which are becoming popular. There are two options to address these gaps: enterprises can ask their current insurers to enter into coinsurance or reinsurance arrangements with cyberinsurance providers to get complete protection from cyberattacks, or they can buy exclusive cyberinsurance contracts from niche cyberinsurance enterprises in the marketplace.

Cyberinsurance Contracts

Even exclusive cyberinsurance contracts have some restrictions on the types of coverage provided. For example, the following losses are not covered by cyberinsurance contracts:

- Loss and damage from unfair trade practices; employment practices; willful, intentional, deliberate, malicious, fraudulent, dishonest or criminal acts; breach of contract; or theft of trade secrets committed by the insured or by thirdparties (i.e., suppliers, partners, service providers) working with the enterprise

- Business losses during unexpected downtime caused by cyberattacks

- Loss of intellectual property (e.g., source code, product designs)

- Loss and damage due to data encryption failure

- Costs related to software upgrades and hardware replacement

- Costs to improve the enterprise’s cybersecurity infrastructure

- Costs related to breach of contractual liabilities by the insured

- Costs related to fines imposed by law enforcement agencies or regulators for crimes committed, policy violations and noncompliance issues

- Injuries to personnel and property damage

- Loss and damage due to acts of foreign governments

- Loss and damage due to violations of consumer protection laws by the insured

- Loss and damage due to online defamation via social media

Figure 2 describes the types of cyberinsurance contracts being sold in the marketplace. Before purchasing cyberinsurance, enterprises should take the following steps:

- Perform a detailed cyberrisk assessment with the help of an expert from the industry and identify the current cyberthreat landscape.

- Review the existing blanket bond insurance contract for any gaps in coverage for the cyberrisk factors identified during the cyberrisk assessment.

- Discuss with the existing insurer the possibility of enhancing the existing contract to include coverage of identified cyberrisk factors.

- If the insurer is not in a position to revise the existing blanket bond insurance contract, search the marketplace for niche insurers and insurance brokers in the industry offering exclusive cyberinsurance plans.

- Evaluate the cybersecurity and data privacy practices of all potential insurers or insurance brokers and identify the most reputable ones. This is very important because enterprises share significant amounts of business-related information with these insurers.

- Discuss with the selected insurers which cyberthreats should be covered by the cyberinsurance plan. Carefully review the plan provided by insurance underwriters for any gaps and misinterpretations. For example, time is critical in ensuring that coverage is triggered appropriately. A policy requiring that a “claim” be made before coverage applies may not be in line with the enterprise’s expectations. Instead, a policy that is triggered upon the “discovery” of a data breach may be more appropriate. Likewise, legal liabilities may be unclear in the plan document. Because insurers are often required to pay out only what is legally required, an enterprise may be liable for outstanding damages that are not covered by insurance. All plan agreements must be carefully read and vetted by the enterprise’s legal counsel.

- Review the details of first- and third-party coverage as coverage limitations may differ from insurer to insurer. Review the plan and negotiate for more coverage if it is deemed inadequate to cover costs payable.

- Review the liabilities section of the plan document carefully. In general, the third-party liabilities section should cover the insured for liability arising from cyberattacks.

- Review exclusions mentioned in the plan documents and negotiate to limit exclusions as much as possible.

- Review the scope of services offered by the insurer as part of the plan.

- Request the removal of sublimits from the policy. If they cannot be removed, negotiate the highest sublimit possible for the lowest cost.

Figure 3 shows the types of protection offered by cyberinsurance products currently sold in the marketplace.

Conclusion

To survive and thrive in the increasingly complex cyberthreat landscape, enterprises should consider cyberinsurance plans. The benefits of these plans extend far beyond mere reimbursement of financial losses. Cyberinsurance plans are evolving into products that help insured enterprises assess their cybersecurity posture and strengthen their incident response capabilities. Cyberinsurance plans are an effective way to build a strong cyberresilience capability. With the arrival of the Fourth Industrial Revolution and significant developments driven by digital technologies such as fintech, blockchain, robotic process automation (RPA) and the Internet of Things (IoT), the possible cyberattack vectors are increasing. Purchasing suitable cyberinsurance plans will help enterprises transfer the responsibility for mitigating these cyberrisk factors to insurers.

Endnotes

1 Clement, J.; “Global Cyber Security and Cyber Insurance Spending 2015-2020,” Statista, 10 November 2020, http://www.statista.com/statistics/387868/it-cyber-securiy-budget/

Vimal Mani, CISA, CISM, Six Sigma Black Belt

Is head of the Information Security Department of the Bank of Sharjah. He is responsible for the bank’s end-to-end cybersecurity program, coordinating its cybersecurity efforts across the Middle East; implementing its cybersecurity strategy and standards; leading periodic security risk assessments, incident investigations and resolution efforts; and coordinating the bank’s security awareness and training programs. He is an active member of the ISACA® Dubai Chapter. He can be reached at vimal.consultant@gmail.com.